Ivy League Endowments Underperform: Is the Yale Model Broken?

Despite recent struggles, the long-term strategy remains strong, but questions linger about hidden risks and market timing.

While 2023 proved rewarding for many investors, Ivy League endowment managers saw lackluster returns, sparking concerns about their renowned investment approach.

Though not disastrous, the latest university investment report reveals average gains of just 2.1% for Ivy League endowments — a far cry from the 11% achieved by a global 70/30 stock-bond benchmark and the impressive 9.8% average of smaller endowments. This underperformance raises questions about the effectiveness of the “Yale Model,” a strategy that has significantly impacted the investing landscape.

When David Swensen took the helm of Yale’s endowment, he dared to disrupt the status quo. Bucking the traditional focus on equities, he pivoted to long-term, real assets, believing endowments with their extended horizons could exploit the inefficiencies of these markets for superior returns. This bold experiment proved immensely successful, becoming the gold standard for asset allocation not just in Ivy League endowments, but across long-term institutional investors globally.

While Ivy League endowments posted slightly better returns in fiscal 2023 compared to the previous year’s losses, their performance still fell short of broader market expectations. On average, these institutions gained only 2.1%, marking an improvement over their 2.4% decline in 2022. However, this pales in comparison to the 14% slump in the standard 70/30 global benchmark. Even Columbia, the top performer among the Ivy League and elite universities (including MIT and Stanford), could only manage a 4.7% return.

The lackluster returns of Ivy League endowments in 2023 can be attributed to two key factors:

1. Venture Capital Slump: Venture capital (VC) faced its worst losses since 2008, with the Cambridge Associates Venture Capital Index plummeting 10.2%. This stands in stark contrast to the Cambridge private equity index, which saw a 6.2% gain. This marks only the third time in history that these two asset classes, both popular with “Yale Model” endowments, have moved in opposite directions.

2. Performance Dispersion: The varying allocations to VC, PE, and public equity significantly impacted individual endowment performance. According to Markov Processes analysis, schools with heavier VC exposure saw lower returns, while those with balanced allocations fared better.

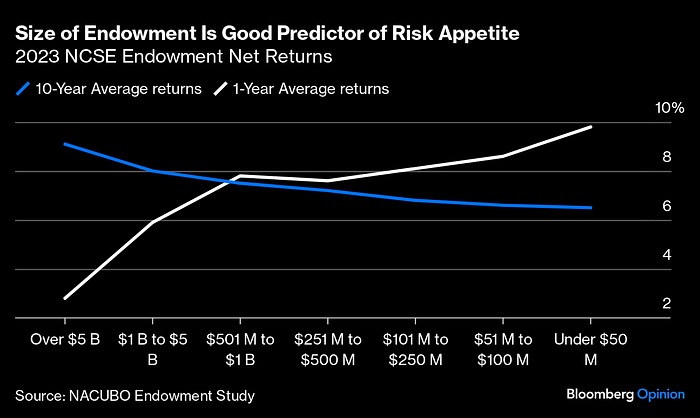

While Ivy League endowments struggled, passively tracking major stock indexes, as advocated by Swensen for individuals, proved highly successful. This strategy, often chosen by smaller endowments due to their resource limitations, usually hurts them in the long run compared to larger funds with more complex strategies. However, in the past fiscal year, this trend reversed. As shown in the chart, the largest endowments, typically boasting superior 10-year returns, underperformed significantly.

Despite Ivy League endowments’ underwhelming 2023 performance, the long-term success of the Yale Model remains undeniable. Ten-year returns remain healthy, and major universities show no signs of abandoning this time-tested strategy. In fact, data from NACUBO indicates a continued focus on alternative investments, with the largest funds increasing their allocations to around 55%, while fixed income remains stable at 19%.

The recent underperformance of Ivy League endowments raises questions about the “Yale Model” and its reliance on riskier investments. While short-term results may fluctuate, historical analysis reveals a clear link between their elevated risk tolerance and long-term success. As MPI points out:

- Over 10 years, Ivy League endowments outperformed a global 70/30 portfolio (6.8% return) with an average return of 9.8%.

- However, they achieved this through significantly more risk compared to the benchmark.

In essence, these endowments act like “levered versions” of a traditional 70/30 portfolio, amplifying both potential gains and losses.

While Ivy League endowments enjoy higher returns than traditional portfolios, their success comes with a price: significantly increased risk. Here’s a breakdown:

- Average Ivy Endowment:

- 12.6% standard deviation (based on reported returns)

- 15.1% estimated volatility (MPI model)

- Nearly 50% more volatile than a global 70/30 portfolio (10.71% standard deviation)

- Top Performers:

- MIT: 11.5% return, 21% modeled volatility (almost double the benchmark’s risk)

- Brown: 11.3% return, 19.8% estimated standard deviation (nearly double the benchmark’s risk)

In simpler terms, Ivy League endowments are like rollercoasters: potentially higher highs but also steeper drops compared to safer investments.

Perhaps the biggest criticism of the Yale Model lies in its private market investments. Unlike publicly traded stocks, these assets are rarely valued in real-time, creating an illusion of lower volatility. However, critics argue that “laundered risk is still risk”. Although private markets might appear less volatile on paper, the potential for large losses remains very real.

In essence, the Yale Model’s focus on private markets masks underlying risk, making some investors question whether elite endowments are actually riskier than a balanced 70% stock portfolio, despite their impressive historical returns.

While 2023 saw certain “hot stocks” outperform traditional strategies, it’s likely an outlier year. Although Ivy League endowments underperformed, they avoided losses entirely. More importantly, on a risk-adjusted basis, the Yale Model still shines compared to its peers.

However, several years like 2023 might be needed to truly test the underlying assumptions of the model and determine its long-term viability in diverse market conditions.